What Are Asset Allocation and Diversification?

• The mixture of different asset classes—including stocks, bonds, and cash—in an investor’s portfolio is called their asset allocation.

• A well-diversified portfolio holds a variety of investments in different asset classes, sectors and parts of the world.

• Asset allocation and diversification are two of the most important ways that investors can manage the amount of risk and volatility in their portfolios.

Much like carpenters need a blueprint before building a home, investors need a plan to pursue their long-term financial goals. That plan typically begins by building a portfolio of investments that will give them the best opportunity to reach those goals. Such a portfolio will provide the investment growth they need while minimizing the risks that their investments will lose value and leave them further from their goals.

Asset allocation and diversification are the two primary tools investors can use to strike a balance between growth and risk. They can help investors answer key questions that arise when building a portfolio, including which types of investments they should hold. Asset allocation and diversification also can help investors understand how to shift their portfolio over time as they move closer to their goals—and in the event that their goals change.

What Is Asset Allocation?

Asset allocation is the mixture of different asset classes in a portfolio. Investors typically hold three primary asset classes as the foundations of their portfolios: stocks, bonds, and cash.

Each asset class has different risk and return characteristics:

• Stocks offer the most growth potential compared to bonds or cash, but also can deliver heavier losses to investors in down markets.

• Bonds are more conservative investments than stocks. They don’t offer the same growth potential, but also don’t carry the same risks of losses (unless the bond issuer defaults or goes bankrupt).

• Cash holdings, which typically include FDIC-insured banking products such as certificates of deposit or savings accounts, are the safest investments. These accounts generally won’t lose value, but the tradeoff is that they offer lower growth potential.

How to Structure a Portfolio

When building a portfolio, investors need to consider two key questions: How much growth they need to meet their long-term financial goals and how much short-term risk they can afford to take on in pursuit of those goals. An investor’s time horizon—the amount of time before they need to access their money—can help answer these questions. The time horizon may measure the time until retirement, or until a child’s college tuition bills start to come due.

In general, the longer the time horizon, the more growth-oriented investments investors can comfortably hold in their portfolio. That’s because they have more time to ride out any short-term fluctuations in investments like stocks. By contrast, investors with just a few years before retirement likely should reduce their exposure to stocks or other riskier investments. That’s because their portfolio may not have enough time to recover in the event of a steep market drop.

An investor’s risk tolerance also matters. Risk tolerance is the amount of risk an investor feels comfortable taking on—an answer that may change over time. For example, if you’re fretting at the thought of a stock market downturn, that’s a sign that you might need to reduce your stock holdings and add more stable investments, such as bonds. Your returns might be lower, but you will likely sleep better at night.

The Importance of Rebalancing

Over time, normal market movements can knock a portfolio’s asset allocation off track. The result: a higher-than-planned allocation to stocks or bonds. For example, if you started with an asset allocation of 60% stocks and 40% bonds, a prolonged bull market may have shifted your allocation to 70% stocks and 30% bonds.

Periodic rebalancing can help investors manage these shifts by bringing the portfolio back to its intended asset allocation. To rebalance, an investor can sell assets that have increased and use the proceeds to buy the asset class that has decreased. Another strategy is to simply devote any new contributions to the part of the portfolio that has lagged.

A portfolio doesn’t need to be rebalanced every time the market moves. A general rule of thumb is to review portfolios a few times a year, or when allocations move beyond their targets by a certain amount—say, 5%.

What Is Diversification?

A diversified portfolio is made up of a variety of investments, including stock and bonds, and different types of investments within those asset classes.

Bonds, for example, can be issued by the US government, corporations, and states or municipalities. Among stocks, shares of big companies are known as large caps for their relatively high market capitalization (stock price times number of shares outstanding). Stocks of smaller companies fall into mid-cap and small-cap categories.

Stocks can also be categorized as growth or value. Growth stocks typically are shares of companies whose earnings or revenue is expected to grow faster than average. Value stocks sell at a bargain in relation to basic measures of company performance, such as earnings, sales, and cash flow.

Having this mix enables investors to benefit from areas of strong performance and provides a cushion when one area of the financial markets performs poorly.

How to Create a Diversified Portfolio

Most investors start building a diversified portfolio using the three main asset classes—stocks, bonds, and cash. They will invest, for example, in small- to large-cap stocks as well as growth and value shares. And they may buy government and corporate bonds.

Additionally, there is another layer of diversification within stocks and bonds. Investors may hold stocks and bonds issued by corporations in different sectors of the economy—including industrials, financials, technology, real estate, and others. They also may diversify internationally, holding a mix of US-based investments as well as investments from other parts of the world. This range of international holdings may include developed markets such as England and Japan and emerging markets such as China, India, and Brazil. Some investors choose to further diversify their portfolios by adding alternative investments such as gold and other commodities.

You also want to diversify by holding more than a handful of individual stocks and bonds. The easiest way to do that is investing through an exchange-traded fund or mutual fund that may hold dozens or even hundreds of different securities.

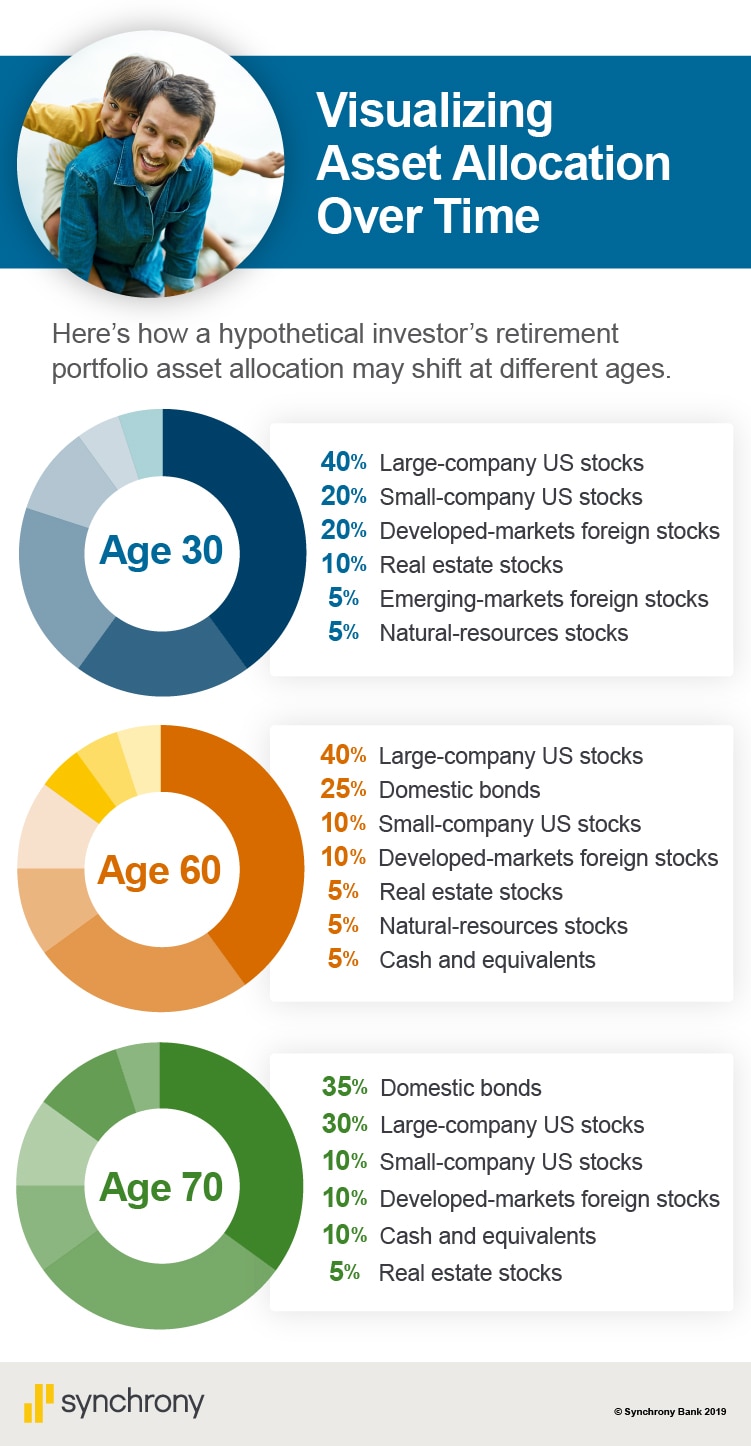

This chart is called Visualizing Asset Allocation Over Time. Here’s how a hypothetical investor’s retirement portfolio asset allocation may shift at different ages. Age 30, 40% Large-company US stocks, 20% Small-company US stocks, 20% Developed-markets foreign stocks, 10% Real estate stocks, 5% Emerging-markets foreign stocks, 5% Natural-resources stocks. Age 60, 40% Large-company US stocks, 25% Domestic bonds, 10% Small-company US stocks, 10% Developed-markets foreign stocks, 5% Real estate stocks,5% Natural-resources stocks, 5% Cash and equivalents. Age 70, 35% Domestic bonds,30% Large-company US stocks, 10% Small-company US stocks, 10% Developed-markets foreign stocks, 10% Cash and equivalents, 5% Real estate stocks.

Using tools such as asset allocation and diversification can help you build a portfolio that fits your needs. These tools offer smart ways to manage risk and volatility inside your portfolio—and can help ensure that your portfolio has the growth potential you need to reach your long-term goals.

T.D. Smith writes about personal finance, investing, and business from Portland, Maine.

This article is part of Synchrony Bank’s Personal Finance Series: Level 301. View all topics in the series here.