First-time home buyers have long considered a down payment of 20% on a mortgage the standard amount. But this initial payment can sometimes be set as low as 5% for a conventional loan—and buyers always have the option of paying more than 20% of the purchase price. So while the “standard” might seem like a no-brainer, it turns out you do need to use your brain on this one.

Factors to Consider

Before you decide to make a 20% (or more) down payment on a house, here’s how to gauge whether your available funds are best used for that purpose:

- If you have high interest debt—like credit cards, for instance—you should pay them down first.

- You should also make sure you are on track for your retirement savings.

The Benefits of a Higher Down Payment

If you’ve gone over the above considerations and it makes sense for you to put down 20% or more, get ready to reap the rewards.

First, letting the seller know you plan to put down more money can give you an edge over other buyers who want to buy the home, because you will appear to be a more serious financial contender. In bidding wars, when sellers or brokers ask for buyers’ “highest and best offers,” the bid with the highest down payment is often considered the “best.”

Borrowers who put down 20% or more don’t have to pay private mortgage insurance (PMI), which either comes with a heavy one-time premium, or carries annual costs to the borrower of between 0.3% and 1.5% of the entire loan.

You’ll also get a better interest rate when you put more of your own money into the deal, according to the Home Buying Institute—and that works out to long-term savings. Plus, you’ll be paying interest on a smaller loan—another way to reduce your overall payments.

Lastly, consider the mortgage interest deduction for first- and second-residence mortgages. If you file as a single person, you can deduct interest on your mortgage up to $375,000. If you file jointly, the deduction is capped at a $750,000 mortgage. This means borrowers are rewarded if they take out smaller loans and make higher down payments. You can use an online calculator to determine your deduction.

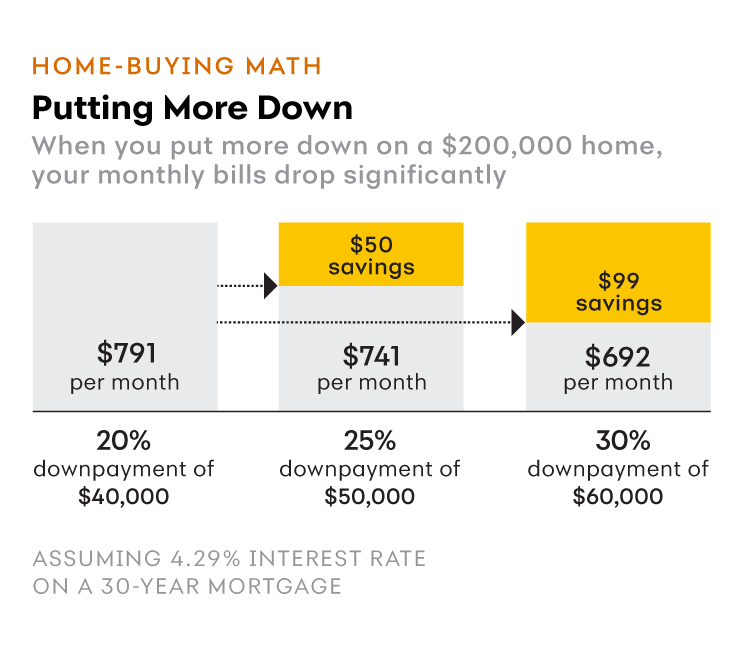

This chart is titled "Home-Buying Math: Putting More Down." If you are buying a $200,000 home, the more money you put down the more your monthly bill drops. The assumption is a 4.29% interest rate on a 30-year mortgage. If you put down 20%, which would be $40,000, your monthly bill would be $791. If you put down 25%, which would be $50,000, your monthly bill would be $741. That's a $50 savings per month. If you put down 30%, which would be $60,000, your monthly bill would be $692. That's a $99 in additional savings. when compared with the 20% down bill.

Colleen Kane is a freelance writer who has written for CNBC, Fortune, Money and many other publications.